Pedal Pushers: When Bikes Became the Vehicle for a Bubble

The comically disproportioned Penny Farthing bicycles were the go-to bike in England during the early 1870s through the early 1880s. However, they were not widely used. Like the bicycles we know today; they were less for daily transportation and more of a novelty item. Penny Farthings were expensive(10 pounds), and they were extremely uncomfortable. They were so uncomfortable that the flagship model was called the “boneshaker”. On top of that the seat was so high they were hard to mount and pedal.

In 1886, John Kemp Starley made the first commercially produced bicycle of a new age of bicycles that transformed the Penny Farthing into something which closely resembles the bikes we ride today. They had a chain in order to reduce the size of the wheel and made them equal sizes. Also, they had pneumatic tires which contributed to a much smoother ride. No to mention the frame was far smaller which made them significantly easier to mount and ride. Because of these features, they received the name “Safety Bikes”.

Similar to the dotcom and other innovation-driven bubbles, technology acted as the spark to ignite a bubble. Many bubbles are associated with technology because of the combination of excitement around innovation, the uncertainty of who will win the market, and the fear of missing out. Going further in many cases innovation-driven bubbles, unlike financial bubbles, can be beneficial in the long run because they develop new technology ecosystems.

With the advent of the safety bicycle, the spark was ignited and the Bicycle Boom was off and running.

Pneumatic Tire Company The Economist “The Sensational offer of £3,000,000 for the business of the Pneumatic Tire Company, to which we referred last week, has had the effect of increasing rampant speculation in cycle shares, which has been more particularly marked in Dublin and in Birmingham.” 25 April 1896

The Boom

Technology drove the bicycle boom. The original bicycles (Penny Farthings) were uncomfortable, hard to pedal, and not practical. Not to mention unsafe. This problem was solved by the safety bike which consisted of three key innovations. First, the lever chain made the wheel turn more times than the bicyclist was actually pedaling. Next, the pneumatic tire or the inflatable tire allowed for more comfort while riding. Finally, the diamond frame was made to connect the two now smaller wheels which made mounting and dismounting much easier. The result of this made the safety bike very similar to the bikes we ride today. The basic design has lasted 130 years and counting, which constitutes a real technological breakthrough.

The industry was a mix of many players from full assembly construction to parts manufacturers. Although many of the new bicycle companies were named after specific parts of the bicycle, for example, the Pneumatic Tire Company and the Chain Lever Company most companies produced the full bike.

The popularity of safety bikes rose quickly and manufacturers promoted their company shares them as much as they could using the 19th-century version of influencers, “Fresh cycle companies are being constantly registered, and investors throughout the country are being deluged with prospectuses, each claiming either an absolutely perfect machine or accessory, or a distinct improvement over anything previously offered to the public.” The Economist 22 May 1897. The new book “Boom and Bust” by William Quinn and John Turner, describes many manufacturers hiring “influencers”, people with strong reputations to endorse the product as well as paying newspapers for their kind words.

For the first years following the invention of safety bicycles they were moderately popular, however, starting 1896 the interest in them skyrocketed. This was around the time of the invention of the diamond frame which made the enjoyment of riding even more accessible.

The original bicycle companies never originally intended to create a bubble; most of the companies simply wanted to raise capital to innovate and improve their product. It was outside tycoons/investors who turned it into a bubble buy using early attempts at leveraged buyouts to try and resell for a higher price this quickly made the industries cost overvalued. Soon many more bicycle companies started popping up and quickly going public.

“The successful floatation of so many cycle companies appears to have imbued the promoting fraternity with a very robust faith in the gullibility of the average British Investor.” The Economist 27 June 1896.

By mid-1896, these companies began to push the boundaries beyond investing in straightforward supply and demand markets. For example, Endurance Tube and Engineering listed on the exchange at £190,000 while neglecting to state whether it had made any profits in the past four years.

Once operators like Ernest Tera Hooley realized the gullibility of investors, they changed tactics and started buying small bicycle manufacturers, taking them private, and making a multitude of empty promises about the products, and then selling shares on the public market. Often, the buying and selling by outside investors proved not to be very profitable because the original buyer had to spend so much on promoting the business that by the time it got to sell there was very little profit margin.

Most bubbles famously occur in major cities like Amsterdam, London, or Paris. However, in the case of the Bicycle Mania, 72 of the more than 175 bicycle companies were in Birmingham a medium-size industrial city, not a financial epicenter. Further, most of the trading of bicycle companies happened on the Birmingham stock exchange. At the same time, the large scale participation was also a major factor which is demonstrated by the fact that 15% of all patents issued at the time were for bicycles.

Source: "Boom and Bust" Quinn and Turner

Investors driven by the excitement of the newly invented safety bikes rushed to invest in bicycle companies. From December 1895 to May 1896 there was a 258% rise in the cycle index. This continued to grow to bubble levels, however, to many investors the delight many bicycle companies moved to other industries where they became very successful.

Meanwhile, as the shares increased in popularity, investors plowed new money into forming numerous companies. The Economist noted in April 1896, “the sensational offer of £3,000,000” for Pneumatic Tyres based primarily on its patents surrounding Dunlop tires. In the second quarter of 1896, the peak of new capital invested in bicycle company shares coincided with the top of the Bicycle bubble share price. It also prefaced the peak of new bicycle company formation a few months later in the first quarter of 1897.

Data Source: Birch's Manual, "Boom and Bust" Quinn and Turner; Graph by Author

Leading up to the collapse, investors were willing to take leaps of faith to buy into the bicycle market. In 1896, the New Premier Cycle Company was formed and floated on the stock exchange at £700,000 despite a prospectus that merely stated its assets were “greater than £100,000.” Capital investment and demand had begun to diverge.

In July 1897, The Economist warned, “As to cycle shares, they will, it is to be feared, turn out to be a very unsatisfactory investment for those who have been induced to take them. Every little metal worker- particularly in Birmingham and Coventry- who could manufacture any of the parts of a cycle appears to have taken advantage of the boom to sell his business to the public., the vast majority of the companies formed recently being of this description. “

By September 1897, the situation worsened, the demand for bicycles in Britain had mostly been satisfied, and American and other foreign cycle makers entered the market. The Economist noted, “The millions of capital were subscribed on the assumption that the high prices current at the time would be maintained, but that delusion has been rudely knocked on the head...those who have profited as cycle shareholders have been vastly outnumbered by those who have been losers"

The Collapse

In April 1898, The Economist profiled two notable Bicycle companies, and showed the current 1898 prices below 60%, though, at the height, Dunlop in particular was considered to have an “unassailable” competitive advantage. While many companies sold bikes and paid dividends, the collapse was in full swing.

While Dunlop indeed introduced groundbreaking innovations, its financial structure including the use of debentures made it a much riskier investment than was obvious just from looking at its products and recent stock prices.

Unlike many other bubbles collapses, the collapse of the Bicycle Mania was mainly contained and in actuality helped other industries by improving upon their technology that consumers wanted. The collapse was also quite slow for a bubble to last until approximately 1907 or about 10 years. Even within some of the companies which participated in the bubble, the damage was fairly minor because many switched industries or others stuck it out because the bicycle industry was still profitable.

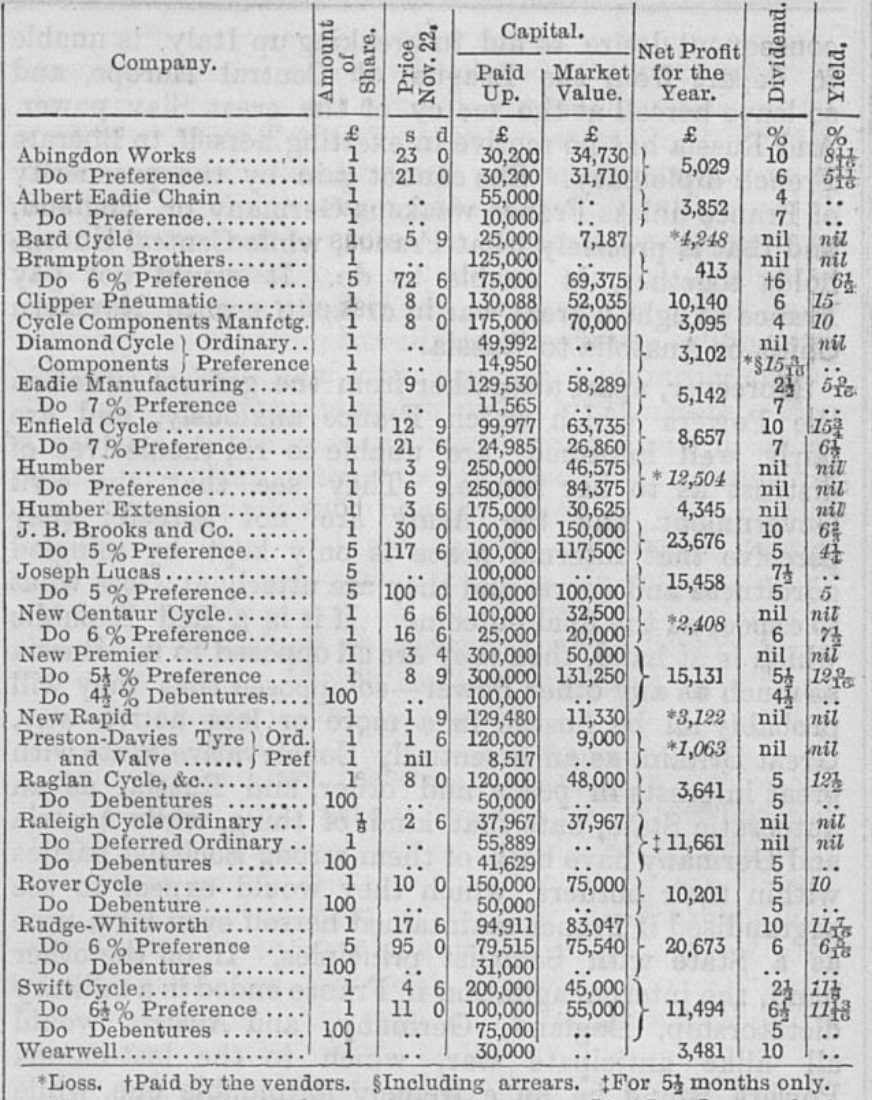

As the collapse continued into 1899, The Economist noted, "The proportion of companies paying dividends on their ordinary capital, 13 out of 23, really conveys a better impression of the year's working than is justified...A more correct idea of the position of the industry is obtained by comparing the net profit with the amount of capital employed." The Economist calculated that average return at 3.5%, rather far off the fever dreams of tech-minded investors. The bicycle shares were well into the collapse phase in 1899, and The Economist points out that companies should have been writing down the goodwill valuation of assets and patents rather than paying out unsustainable dividends.

Cycle Companies In Bubble Collapse Era, 1898-9, Saturday, Nov. 25, 1899

Publication: The Economist

One of the most surprising facts about the bicycle mania is that all things considered it was beneficial to the British economy overall and their economic development. This is because the companies brought new products that consumers liked and technology and that subsequently became crucial in the foundation of other industries. For example, the bicycle companies went on to lead construction, motor car, motorcycle industries, aircraft, and ball bearings manufacturing.

Technology changes the way people see an industry or industries in this case the act of making cycling more accessible through new technology made it a “hot” industry. There are financial risks when investors get over-excited at new technologies and turn them into bubbles. However, if the tech is legit, then there are usually long term winners like Amazon and Google emerging from the dotcom bubble. This is different from purely financial bubbles that do not leave technological improvements in their wake after they pop.

After the Bicycle Bubble, there were a few businesses that lived on to be “house-hold” names most of these were companies that switched industries to pursue success. One of the most notable of these companies is Dunlop Tire the famous car tire manufacturer was originally named the Pneumatic Tire Company and started during the bubble as a bicycle manufacturer.

Rudge Whitworth helped create both the motorcycle and sports car wheel industries. The most impressive endurance record by far is the Raleigh Bicycle company which started during the boom of the industry and is still around producing bicycles today.

One of the most interesting pieces of this bubble is not what makes it similar to other bubbles, but what separates it. Unlike most bubbles or manias the bicycle mania had a slow decline of about ten years. This was caused by some bicycle manufacturers switching to other fields and the demand for bicycles still being consistent. This is different from other bubbles like the South Sea bubble where there wasn’t a product which made it far more volatile. This bubble or mania was overall beneficial to Britain and the world from a technological and industrial developmental standpoint. This is because it allowed for new innovations and creations like the ball bearing which allowed the industrial world to literally work more smoothly and efficiently.

Twitter - @soreninvesting

Comments

Post a Comment